Secure Document Sharing

Secure Document Sharing

Top 7 Most Common Estate Strategy Mistakes

Top 7 Most Common Estate Strategy Mistakes (and How to Avoid Them)

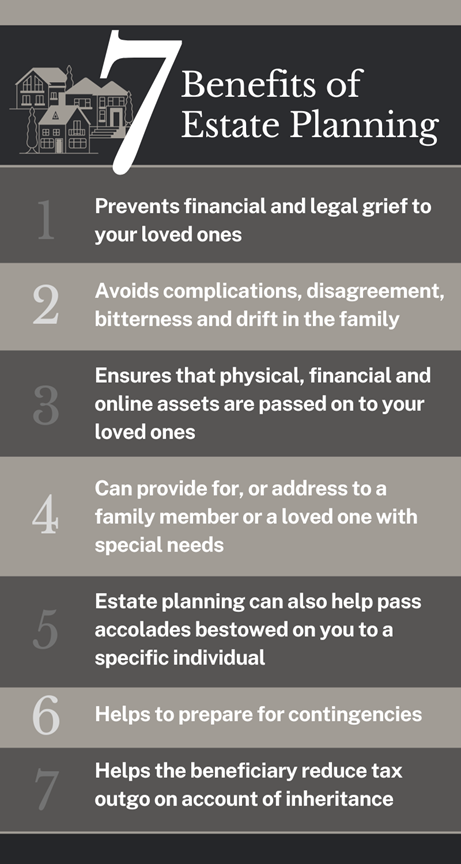

Getting your affairs in order and outlining what you want done with your estate after you’re gone is one of the greatest gifts you can leave your loved ones. However, not preparing for the transfer of your assets can lead to confusion, potential family disputes, and outcomes that don’t align with your ultimate wishes.

Creating a financial strategy that considers how an estate is structured is one of the most important services we provide as financial professionals. Over the years, we’ve helped guide many of our clients so they can make sound estate decisions and potentially avoid any missteps.1,2

1. Failing to create a comprehensive estate strategy

One of the biggest financial mistakes is not developing a strategy for your estate. Some people never get around to it, while others think that estate concerns are only for the wealthy. Without a strategy, your assets may not be distributed based on your wishes, and your heirs may be forced to make hard decisions at a difficult time for your family.

It’s important to understand the difference between various tools that can help manage an estate, such as a healthcare power of attorney. Your estate strategy also should consider any business agreements, prenuptial agreements, and other directives to help ensure they all work together.

2. Not updating an estate strategy periodically

Failing to update your estate strategy periodically can lead to unintended consequences. An outdated strategy may not reflect your current wishes or circumstances, nor incorporate all your assets or beneficiaries.

Consider reviewing your estate strategy every three to five years, or when your personal circumstances change, e.g., births, deaths, marriages, or divorces. Also, you may want to revisit your estate strategy if changes occur in your business life, e.g., a new property acquisition. You may want to use “trigger events,” e.g., milestone birthdays, as reminders to review your strategy.

3. Not considering taxes

Underestimating your potential tax liability can put your heirs in a difficult position. Keep in mind that this article is for informational purposes only and isn’t a replacement for real-life advice. Your tax or legal professional should be able to address questions about your potential estate taxes.

4. Not taking advantage of charitable giving

Not using charitable giving can result in missed opportunities to support important causes, reflecting on you and your legacy.

Philanthropy can be part of your overall estate discussion. You then can develop a charitable giving strategy that aligns with your values and goals. In addition to cash gifts, myriad tools are available that may offer other benefits to your estate.

5. Failing to account for business succession

If you own a business, consider how your business factors into your estate strategy to ensure a smooth transition.

Developing a business succession approach can help you manage the process. One way to help safeguard a business is to create a buy-sell agreement, which is a contract between different entities within a corporation to buy out a deceased or disabled member’s interests. Various buy-sell agreements and ways to fund the contract can be employed.

6. Not communicating with heirs

Not discussing estate decisions and intentions with heirs can lead to misunderstandings, and in extreme circumstances may lead to legal challenges.

To help avoid this mistake, communicate openly and honestly with your heirs about your estate strategy decisions and intentions, and involve them in the process to the greatest extent possible. While it may be a hard conversation to start, it’s critical for all involved.

7. Not asking for help with difficult estate decisions

A poorly constructed estate strategy can result in mistakes and missed opportunities. Consider working with professionals who help families create estate strategies; they can anticipate issues that you may overlook.

In some situations, an estate team should comprise your financial professional, attorney, and tax advisor. A tax advisor brings knowledge about estate taxes to the conversation, while an attorney can help create the critical documents needed to support your estate strategy. As financial professionals, we often function as estate team quarterbacks, coordinating activities and ensuring that critical areas are being addressed and that everyone is on the same page.

Also, a team of professionals can help examine your estate from different perspectives. For example, if the team determines that a trust may be appropriate, you’d have access to professionals familiar with the laws that must be followed to create a trust document.

Another benefit from having outside assistance with your estate is that tax laws change constantly, so having a team may help you keep your documents up to date. For example, several estate provisions in the Tax Cuts and Jobs Act are set to expire on December 31, 2025. You may want your team to consider how your current estate strategy could be affected if the laws revert back to 2017.

The best time to start your estate strategy discussion is right now.

Facing one’s mortality is never easy, but ignoring the inevitable doesn’t help anyone. Failing to address these common estate issues can have consequences for your heirs. We’ve seen what happens when estates are neglected, and we confidently can say that taking the necessary steps now may be more helpful than you can imagine to those whom you care about most.

1. NationalLawReview.com, 2023

2. FindLaw.com, April 24, 2023